As the real estate market has cooled off in many parts of the country, investing in property may seem wise in the long run. But taxes can be a significant concern.

Owning real estate in a C corporation may not be wise when considering taxes because it puts you at risk of being double-taxed.

This means that if you sell the property and make a profit, the gain may be subject to taxation twice—once at the corporate level and again at the shareholder level when the corporation pays out profits to shareholders as dividends.

The Tax Cuts and Jobs Act reduced the double taxation threat, but with our current federal debt, you face the risk that lawmakers will hike the corporate tax rates and possibly also tax dividends at higher ordinary income rates.

To avoid this threat, I usually recommend using a single-member LLC or revocable trust to hold real property. A disregarded single-member LLC delivers super-simple tax treatment combined with corporation-like liability protection, while a revocable trust can avoid probate and save time and money.

If you are a co-owner of real property, it is advisable to set up a multi-member LLC to hold the property. The partnership taxation rules that multi-member LLCs follow have several advantages, including pass-through taxation.

In conclusion, holding real property in a C corporation can expose you to the risk of double taxation, and I don’t recommend it. Instead, consider a single-member LLC, revocable trust, or multi-member LLC, depending on your situation.

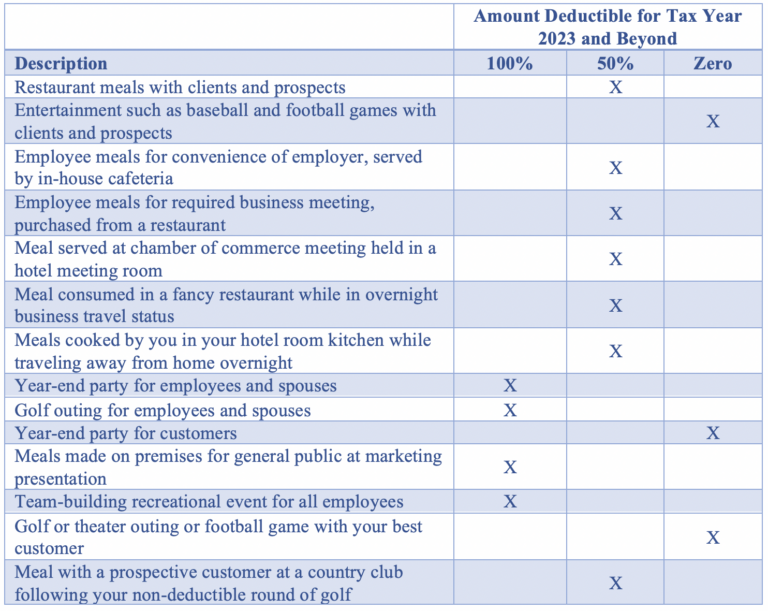

Helicopter View of 2023 Meals and Entertainment

As you may already know, there have been some major changes to the business meal deduction for 2023 and beyond. The deduction for business meals has been reduced to 50 percent, a significant change from the previous 100 percent deduction for business meals in and from restaurants, which was applicable only for the years 2021 and 2022.

To help you better understand the current situation, see the table below:

Are You a Regular Investor or a Tax-Favored Securities Trader?

As we navigate the recent volatility in the stock market, you may want to think about the possible favorable federal income tax treatment the tax code gives to a securities trader.

Suppose you can qualify as a securities trader for federal income tax purposes. In that case, you deduct your trading-related expenses on Schedule C of Form 1040 and make the taxpayer-friendly mark-to-market election, which is not available to garden-variety investors.

The mark-to-market election has two important federal income tax advantages:

- Exemption from the capital loss deduction limitation

- Exemption from the wash sale rule

But there is a price to pay for these tax advantages. As a trader who has made the mark-to-market election, you must pretend to sell your entire trading portfolio at market on the last trading day of the year, which may have little or no tax impact if you have little or nothing in your trading portfolio at year-end.

Your trading activities must constitute a business for you to qualify as a securities trader, and you must meet both of the following requirements:

- Your trading must be frequent and substantial.

- You must seek to profit from short-term market swings rather than longer-term strategies.

If you are a calendar-year taxpayer, the deadline to make the mark-to-market election for your 2023 tax year is April 18, 2023 (that’s right around the corner). You make the election by including a statement with your 2022 Form 1040 filed by that date or with a Form 4868 extension request for your 2022 return filed by that date.

Avoid This Family-Member S Corporation Health Insurance Mistake

There are two important issues related to health insurance deductions for S corporations.

First, if you own more than 2 percent of an S corporation, there are three steps you need to follow to claim a deduction for health insurance:

- Step 1. The cost of the insurance must be on the S corporation’s books.

- Step 2. The corporation must include the cost of the health insurance premiums on your W-2 form as taxable income (but not subject to payroll taxes).

- Step 3. If eligible, you must claim the health insurance deduction as an above-the-line deduction on Schedule 1 of Form 1040.

Second, this three-step procedure applies to your spouse, children, grandchildren, great-grandchildren, parents, grandparents, and great-grandparents if they work for your S corporation and the corporation covers them with health insurance.

The three rules apply to the relatives listed above who work in the S corporation, even if they don’t own any stock directly. For health insurance purposes, the tax code attributes your stock ownership to them and deems that they own what you own.

It’s crucial to get this right, as failing to do so could result in a lost health insurance deduction for your family members and zero deductions or the S corporation.

If you or your S corporation did not handle this correctly in the past, you need to amend the returns to ensure that you create and protect the proper tax deductions.